Built to Last, Not to Sell: The Portuguese Business Mindset

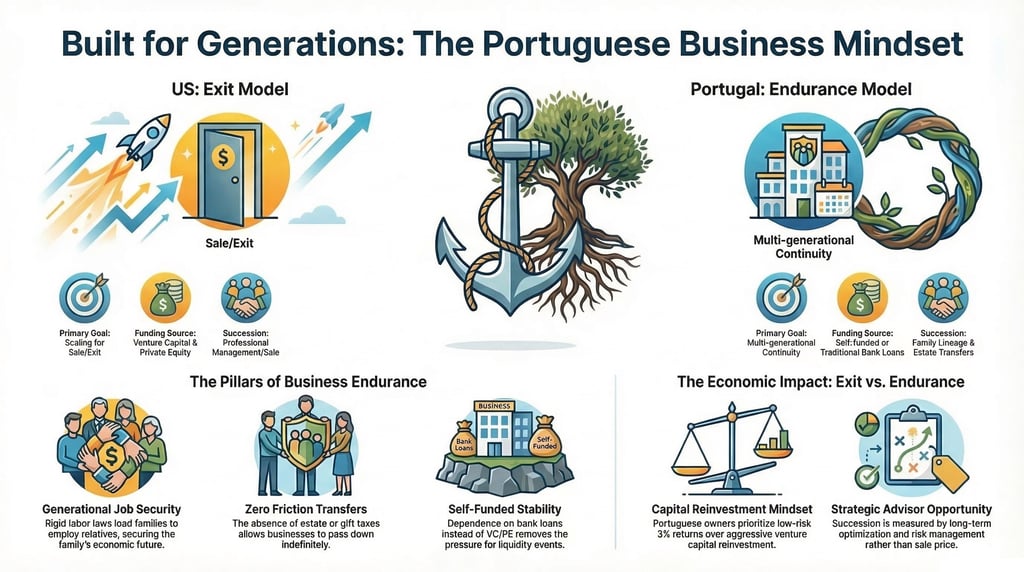

In the U.S., the business playbook is simple: you build it, you scale it, and you exit. But here in Portugal? Companies aren't built for the exit. They’re built for endurance. And when you look at the underlying market mechanics, it makes perfect sense why families hold onto these businesses across generations

Being an investment banker in Portugal must be a relatively quiet existence, simply because there isn't a whole lot for them to do. In the U.S., the ultimate endpoint for a successful business is almost always a sale. You build it, you scale it, you exit. Here in Portugal, that endpoint is far less clear. In fact, I’m not convinced a conventional endpoint even exists for most of these companies.

For anyone in valuation and strategy, that completely shifts the landscape. The real opportunity here isn't necessarily in plain vanilla business valuation for M&A; it's in strategic advising. While the US market is engineered to push founders toward the exit, the Portuguese market is fundamentally built for endurance. Families here hold onto businesses across generations, and when you look at the underlying data and market mechanics, there are a few very pragmatic reasons why.

First, you have to look at the labor market. It's notoriously difficult and expensive to fire someone in Portugal, which makes companies incredibly cautious about hiring in the first place. For a family, the most reliable way to secure their economic future, and to guarantee their members a livable wage, is to just employ them in the family business. It even takes the place of the classic US teen summer job, which just isn't a pervasive cultural fixture here.

Combine that labor dynamic with the fact that Portugal has no estate or gift tax, and there’s absolutely no friction stopping families from passing these businesses down indefinitely. As a result, multigenerational family businesses and family offices are the absolute bedrock of the economy. It’s not unusual to see commercial buildings held by the exact same family since the fascist or even monarchist eras, or vineyards that have remained in the same bloodline for centuries. It's just a conventional part of the economic landscape.

Then there’s the capital side of the equation. In the States, if you sell your business for a windfall, the next steps are obvious. You dump a chunk of it into the stock market, maybe start an angel fund, and suddenly you're a venture capitalist. But the retail investment mindset in Portugal, and much of Europe for that matter, is completely different. They optimize for minimal risk. A successful exit usually means parking cash somewhere safe for a 3% return, which, let's be honest, barely offsets inflation. There’s no cultural playbook that says you should cash out and start writing checks to startups.

Furthermore, the pressure to exit just isn't there because the capital structure doesn't demand it. The overwhelming majority of Portuguese businesses are self-funded or propped up by traditional bank loans. You don't have private equity or venture capital investors sitting on the cap table, banging on the boardroom door, and demanding a liquidity event.

From a macroeconomic perspective, this lack of an exit market is a double-edged sword. An active business exit market is a hallmark of a dynamic economy. Exits create market liquidity, broaden the base of investable funds, and actively encourage outside capital because investors can clearly see their path to a return. The Portuguese model inherently lacks that velocity. But as an advisor, that's not a systemic issue I can fix. What the status quo does do, however, is offer some incredibly intriguing opportunities to help these long-term businesses optimize their strategy, manage their risk, and figure out how to thrive for their next hundred years.

Terms and Conditions

Portugal Address

Prontos Impact Village

Largo Heróis da Naulila nº 16, Loja 22

2500-107 Caldas Da Rainha, Leiria

Portugal

United States Address

1441 Woodmont Ln NW, Suite 2028

Atlanta GA 30318

United States Of America